What I Wish I Knew Before Switching Careers: My First Steps With Investment Tools

Changing careers felt like jumping off a cliff—exciting, but terrifying. I had no safety net, and my savings were shrinking fast. That’s when I realized: if I didn’t start growing my money, I’d run out before finding my new path. I began exploring simple investment tools, not to get rich, but to stay afloat. What I learned changed everything—how to protect what I had, grow it slowly, and avoid costly mistakes. This is what I wish I’d known earlier.

The Breaking Point: Why I Started Looking at Investments

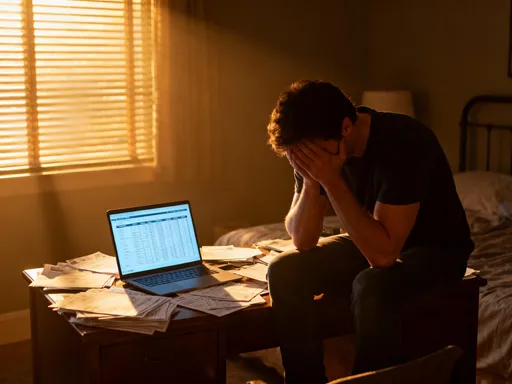

There was a moment, about three months into my career transition, when I sat at my kitchen table staring at my bank statement and felt my chest tighten. The numbers were moving in the wrong direction—down. I had left a stable job in marketing to pursue a certification in health and wellness coaching, a field I was passionate about but one that wouldn’t pay me for at least six months. I had saved what I thought was enough, but unexpected costs—course fees, laptop upgrades, even higher grocery bills from working from home—were adding up. I wasn’t reckless, but I hadn’t planned for how quickly my savings could erode without income flowing in.

That night, I made a decision that changed my financial trajectory. Instead of just cutting back—skipping dinners out, canceling subscriptions, and driving less—I realized I needed to make my money work for me. Saving was no longer enough. I needed growth. I needed my money to do more than sit idle. This wasn’t about chasing wealth or retiring early. It was about survival. I needed a financial cushion that could last through uncertainty, and I realized that passive income and smart investing could be part of the solution, even on a modest scale.

For years, I had treated investing as something for people with extra cash—people who had already “made it.” I thought you needed thousands to start, or a finance degree to understand what you were doing. But my situation forced me to challenge those assumptions. I began to see that investing isn’t just for the wealthy or the mathematically gifted. It’s a tool for anyone who wants to protect their future, especially during life transitions. And for someone in the middle of a career shift, that protection is not a luxury—it’s a necessity.

What I didn’t know then was how many beginner-friendly options existed. I assumed the stock market was too risky, that mutual funds were too complex, and that financial advisors were too expensive. But as I dug deeper, I discovered that there were accessible, low-cost ways to start small and grow steadily. That shift in mindset—from seeing investing as out of reach to seeing it as a practical safety measure—was the first real step toward financial resilience.

First Moves: Choosing Beginner-Friendly Investment Tools

My first real step into investing began with fear—fear of making the wrong choice, fear of losing money, fear of looking foolish. I remember opening a brokerage account online and being overwhelmed by the options: ETFs, mutual funds, individual stocks, bonds, REITs. The terminology alone felt like a foreign language. I didn’t want to dive into deep waters. I needed a shallow end where I could learn to swim without drowning.

That’s when I discovered index funds. These are investment vehicles that track a specific market index, like the S&P 500. Instead of trying to pick winning stocks, which is extremely difficult even for professionals, index funds allow you to own a small piece of hundreds of companies at once. They are diversified, low-cost, and historically have delivered solid long-term returns. What made them perfect for me was their simplicity and accessibility. I could start with as little as $50, and many platforms offered automatic investments, so I could set it and forget it.

Alongside index funds, I explored robo-advisors—digital platforms that create and manage a portfolio for you based on your goals and risk tolerance. I liked that they removed the emotional component of investing. No panic selling during market dips, no impulsive buys based on news headlines. The algorithm did the work, rebalancing my portfolio periodically and keeping fees low. It felt like having a financial advisor without the high price tag. I started with a small amount—$200—and gradually increased my contributions as I gained confidence.

Another tool that became part of my foundation was the high-yield savings account. While not an investment in the traditional sense, it offered a safe place to park emergency funds while earning significantly more interest than a regular savings account. At the time, I was earning less than 0.5% in my old bank, but I found online banks offering over 4%. That might not sound like much, but on a $5,000 emergency fund, it meant an extra $200 per year—money I wasn’t earning before. It was a small win, but it showed me that even conservative tools could make a difference.

What tied all these tools together was their low barrier to entry. They didn’t require large sums, expert knowledge, or constant monitoring. I could start small, learn as I went, and adjust as my situation changed. That flexibility was essential during a time when my income was unpredictable and my focus was on retraining. These tools didn’t promise overnight riches, but they offered something more valuable: peace of mind.

Why Safety Matters More Than Returns (Especially Now)

Early in my journey, I almost made a costly mistake. A friend told me about a “guaranteed” return investment—an online platform promising 12% annual returns with no risk. It sounded too good to be true, and it was. I nearly transferred $1,000 before I paused and did more research. A quick search revealed warnings from financial regulators and user complaints about delayed withdrawals and hidden fees. I backed out just in time. That experience taught me a hard lesson: when you’re in a vulnerable financial position, safety must come before returns.

During a career transition, your risk tolerance changes. You don’t have the luxury of waiting years to recover from a loss. Every dollar counts. That’s why preserving capital—the money you’ve already saved—should be your primary goal. Chasing high returns might work for someone with a stable income and a long time horizon, but for someone like me, who was months away from needing every penny, it was a dangerous game.

I learned to evaluate investments not by how much they could earn, but by how much I could afford to lose. Index funds and robo-advisors, while not immune to market fluctuations, are diversified and historically resilient. Even in downturns, they tend to recover over time. High-yield savings accounts, while offering lower returns, protect your principal and provide liquidity. These tools may not make headlines, but they build stability—the kind of stability that lets you focus on your career goals without constant financial anxiety.

Emotional decision-making is one of the biggest risks in investing. Fear and greed can lead to panic selling or reckless buying. I’ve felt both. There was a market dip six months after I started, and my account balance dropped 10%. My first instinct was to pull everything out. But I remembered my goal: long-term growth, not short-term gains. I stayed the course, and within a year, my portfolio had recovered and even grown. That experience taught me the value of discipline and patience. Investing isn’t about timing the market; it’s about time in the market.

Today, I measure success not by how high my returns are, but by how calm I feel when I check my accounts. I sleep better knowing my money is in reliable, low-cost tools that align with my risk tolerance. That sense of security didn’t come from chasing big wins—it came from prioritizing safety, avoiding unnecessary risks, and trusting a consistent strategy.

Building a Cushion: How Investments Became My Backup Plan

One of the most powerful shifts in my thinking was seeing investments not as a distant retirement plan, but as an active part of my financial safety net. In the past, I viewed retirement accounts as untouchable—something I wouldn’t access for decades. But during my career change, I needed access to funds that could support me in the near term. I realized I could structure my investments to serve dual purposes: growth and emergency backup.

I divided my savings into layers. The first layer was my emergency fund—three to six months of living expenses—held in a high-yield savings account. This money was completely liquid, meaning I could access it anytime without penalties. The second layer was my investment portfolio, held in a taxable brokerage account. This included index funds and ETFs, which I didn’t plan to touch for at least three to five years. Because I wasn’t relying on this money immediately, I could accept some volatility in exchange for higher growth potential.

This two-tier approach gave me both flexibility and protection. If my certification program took longer than expected, or if I had unexpected medical bills, I had access to cash without derailing my long-term goals. At the same time, the money I wasn’t using was working for me, compounding over time. I wasn’t just surviving—I was building resilience.

Another benefit of this structure was psychological. Knowing I had a backup plan reduced my stress and gave me the confidence to take calculated risks in my career. I could say yes to an unpaid internship, invest in additional training, or wait for the right job offer instead of settling for the first one that came along. My investments weren’t generating huge income yet, but they were buying me time—and time is one of the most valuable assets during a transition.

Over time, I began to see my financial plan as a living system, not a static set of rules. I adjusted my contributions based on my cash flow, rebalanced my portfolio when needed, and reviewed my goals regularly. This wasn’t about perfection—it was about progress. And every small decision added up to greater security and freedom.

Learning on the Fly: Free Resources That Actually Helped

I didn’t have the time or money to go back to school for finance, so I turned to free, reliable resources to build my knowledge. I started with podcasts—audio programs I could listen to while cooking, commuting, or folding laundry. One that stood out was “The Basic Investing Podcast,” which explained concepts like compound interest, asset allocation, and dollar-cost averaging in plain language. I didn’t understand everything at first, but over time, the ideas began to click.

I also explored free online courses from reputable institutions. Coursera and edX offered introductory finance classes from universities like Yale and the University of Illinois. These weren’t quick fixes, but they gave me a solid foundation. I learned how inflation erodes savings, why diversification reduces risk, and how taxes affect investment returns. Most importantly, I learned to ask better questions—questions that helped me evaluate tools and avoid scams.

Mobile apps also played a big role. Many brokerage platforms have built-in educational centers with short videos, articles, and quizzes. I spent 15 minutes a day learning one new concept. Over six months, that added up to dozens of hours of learning. I also used budgeting apps to track my spending and set savings goals, which helped me free up money to invest.

What made these resources effective was their accessibility and consistency. I didn’t need to be a full-time student. I could learn in small chunks, at my own pace. And because the content came from trusted sources, I didn’t waste time on misinformation. I also joined online communities—forums and Facebook groups—where beginners shared experiences and asked questions. Reading about others’ mistakes helped me avoid making the same ones.

Self-education didn’t make me an expert, but it gave me confidence. I stopped feeling like I needed a financial advisor to make every decision. I still consult professionals when needed, but now I can have informed conversations. I know the basics, I understand the risks, and I can evaluate options on my own. That independence has been one of the most empowering parts of my journey.

Avoiding the Traps: Common Mistakes I Almost Made

As a beginner, I was vulnerable to mistakes—some obvious, some subtle. One of the most common traps is hidden fees. I almost signed up for a managed investment account that charged a 2% annual fee. At first, that didn’t seem like much, but I later learned that over 20 years, a 2% fee could eat up nearly 30% of my returns. That’s why I now prioritize low-cost index funds and robo-advisors with transparent fee structures. A 0.25% fee may not sound like a big difference, but over time, it can mean thousands of dollars saved.

Another trap is over-diversification. In an effort to reduce risk, I considered investing in ten different funds, thinking more was better. But I learned that too many investments can dilute returns and make tracking difficult. True diversification doesn’t mean owning everything—it means owning a mix of asset classes that respond differently to market conditions. I simplified my portfolio to a few core funds: one U.S. stock index, one international stock index, and one bond fund. That gave me broad exposure without unnecessary complexity.

I also had to resist the temptation of “easy money” schemes. From cryptocurrency hype to real estate seminars promising passive income, there were constant distractions. I learned to ask three questions before any investment: Is it regulated? Do I understand how it works? Can I afford to lose the money? If I couldn’t answer yes to all three, I walked away. That simple filter saved me from several potential losses.

Finally, I almost made the mistake of checking my account too often. In the beginning, I logged in daily, watching every up and down. That led to anxiety and the urge to make impulsive changes. I realized that short-term fluctuations are normal and that constant monitoring only increases stress. Now, I review my portfolio quarterly. I rebalance if needed, but I don’t react to daily noise. That discipline has helped me stay focused on my long-term goals.

Putting It All Together: My Simple Strategy for Stability and Growth

Today, my financial strategy is simple, sustainable, and aligned with my life goals. I contribute automatically to a mix of low-cost index funds through a robo-advisor, which handles rebalancing and tax efficiency. I keep my emergency fund in a high-yield savings account, separate from my investing accounts. I review everything once a quarter, adjusting only when my goals or circumstances change. I don’t expect to get rich, but I do expect to be prepared.

This system didn’t happen overnight. It grew from trial, error, and learning. I made small choices—starting with $50, reading one article a week, asking for help when confused—and over time, those choices built a foundation of stability. I now have a financial cushion that supports my career, reduces stress, and gives me the freedom to take thoughtful risks.

More than the money, I’ve gained confidence. I no longer feel helpless when the market dips or when my income fluctuates. I have a plan, and I trust it. That peace of mind is worth more than any return percentage. For anyone considering a career change—or any major life shift—I offer this advice: don’t wait to start investing. You don’t need a lot of money, a finance degree, or perfect timing. You just need to begin, with tools that are safe, simple, and within reach. Your future self will thank you.